Navigating tax season can be a daunting task, but employing strategic planning can lead to impressive savings. By focusing on deductions, investments, and credits, individuals can significantly lower their tax liabilities. Additionally, incorporating unique marketing approaches, such as promotional bag ideas, can enhance visibility and foster better financial outcomes in the long run.

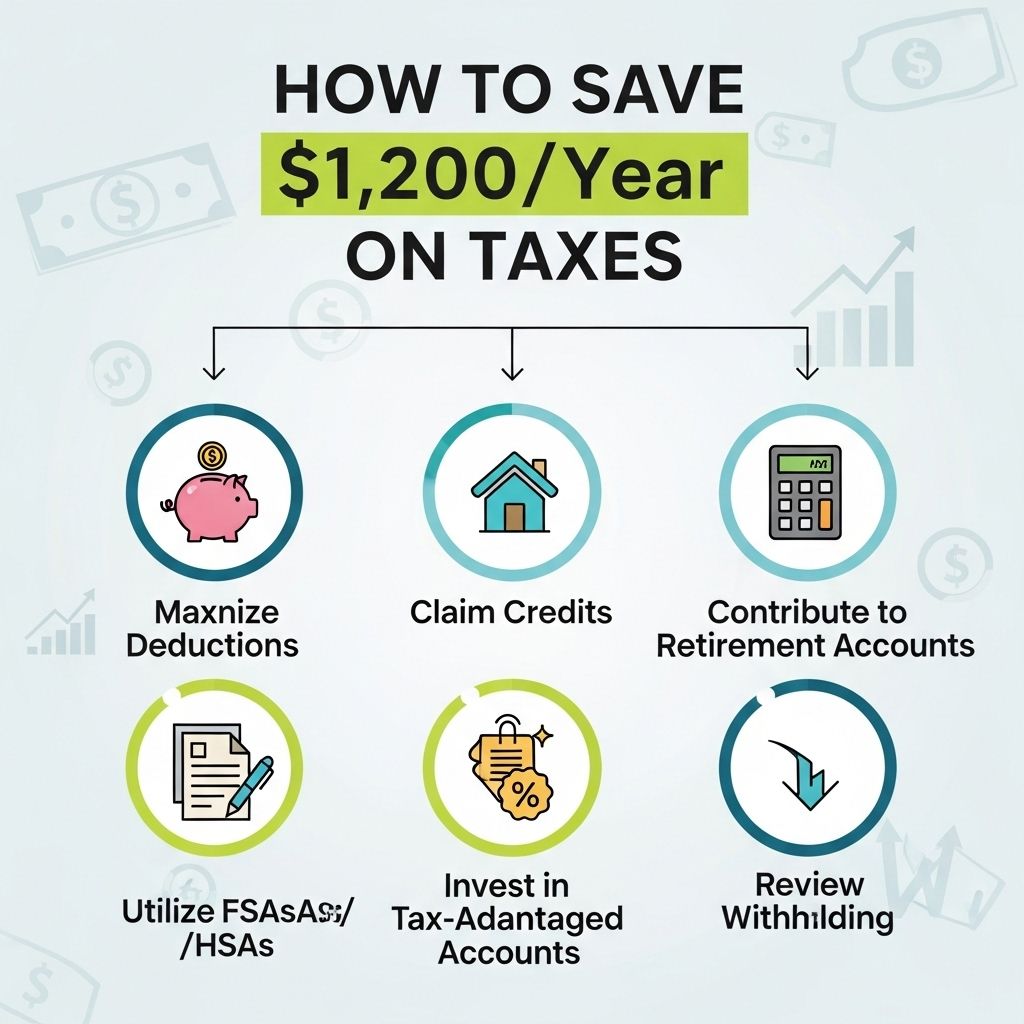

Tax season can be a stressful time for many individuals, especially when it comes to finding ways to minimize liabilities and maximize returns. However, with the right strategies and a little bit of planning, it is possible to save significant amounts on taxes each year. In this article, we will explore effective strategies to help you save $1,200 annually on your tax bill.

Deductions: Maximizing Your Write-Offs

One of the most straightforward ways to reduce your taxable income is by taking advantage of various deductions. Deductions lower the amount of income that is subject to tax, ultimately reducing your tax bill.

Common Tax Deductions

- Standard Deduction: For 2023, the standard deduction is $13,850 for single filers and $27,700 for married couples filing jointly.

- Itemized Deductions: If your total deductions exceed the standard deduction, consider itemizing. Common itemized deductions include:

- Mortgage interest

- State and local taxes

- Medical expenses that exceed 7.5% of AGI

- Charitable contributions

Keep Track of Your Expenses

To effectively utilize itemized deductions, maintain meticulous records of all relevant expenses throughout the year. This can include:

- Receipts for charitable donations

- Medical bills

- Property tax statements

- Mortgage interest statements

Retirement Contributions: A Dual Benefit

Investing in retirement accounts not only prepares you for the future but can also provide immediate tax benefits. Contributions to certain retirement accounts can lower your taxable income, providing substantial savings.

Types of Retirement Accounts to Consider

| Account Type | Tax Treatment | Contribution Limit |

|---|---|---|

| Traditional IRA | Contributions may be tax-deductible | $6,500 ($7,500 if age 50 or older) |

| 401(k) | Pre-tax contributions reduce taxable income | $22,500 ($30,000 if age 50 or older) |

| Roth IRA | Contributions are not tax-deductible, but qualified withdrawals are tax-free | $6,500 ($7,500 if age 50 or older) |

Utilizing Tax Credits

While deductions reduce taxable income, tax credits directly reduce the amount of tax owed. There are numerous tax credits available, some of which can lead to significant savings.

Types of Tax Credits

- Earned Income Tax Credit (EITC): A refundable tax credit for low-to-moderate-income working individuals and families.

- Child Tax Credit: Provides a credit of up to $2,000 per qualifying child.

- Education Credits: These include the American Opportunity Credit and the Lifetime Learning Credit for qualified education expenses.

Health Savings Accounts (HSAs)

Health Savings Accounts offer another opportunity for tax savings. Contributions to HSAs are tax-deductible, and distributions used for qualified medical expenses are tax-free.

Benefits of HSAs

- Tax-deductible contributions

- Tax-free growth

- Tax-free withdrawals for qualified medical expenses

For 2023, the contribution limits for HSAs are:

- $3,850 for individuals

- $7,750 for families

Tax-Loss Harvesting

If you have investments, tax-loss harvesting can be a beneficial strategy. This involves selling investments at a loss to offset capital gains and reduce your tax liability.

How to Implement Tax-Loss Harvesting

- Identify losing investments that you can sell.

- Sell these investments to realize the losses.

- Reinvest the proceeds in similar but different investments to maintain your portfolio balance.

Plan for the Future: Tax Strategies

Long-term planning can help you optimize your tax situation over the years. Consider the following strategies:

Adjust Your Withholding

Review your W-4 form to ensure that the correct amount of tax is being withheld from your paycheck. Adjustments can help to avoid overpaying taxes throughout the year.

Consult with a Tax Professional

Engaging a tax professional can provide personalized strategies tailored to your specific financial situation. They can identify deductions and credits you may have overlooked, ultimately helping you save more on your taxes.

Conclusion

By implementing these strategies, you can effectively save $1,200 or more each year on your tax bill. From maximizing deductions and utilizing tax credits to making smart investment decisions, proactive tax planning can significantly impact your financial health. Start early, keep accurate records, and consult with professionals to ensure you are taking advantage of all available tax-saving opportunities.

FAQ

How can I save $1,200 a year on taxes?

You can save $1,200 a year on taxes by maximizing your deductions, contributing to retirement accounts, and utilizing tax credits.

What deductions can I claim to reduce my taxable income?

Common deductions include mortgage interest, student loan interest, medical expenses, and state and local taxes paid.

Are there specific tax credits I should be aware of?

Yes, some valuable tax credits include the Earned Income Tax Credit, Child Tax Credit, and education credits like the American Opportunity Credit.

How can retirement accounts help me save on taxes?

Contributing to retirement accounts like a 401(k) or IRA can lower your taxable income, allowing you to save on taxes now and grow your savings for the future.

Is it beneficial to consult with a tax professional?

Yes, a tax professional can help you identify potential deductions and credits you may not be aware of, maximizing your tax savings.

What are some common mistakes to avoid when filing taxes?

Avoid common mistakes like missing deadlines, overlooking deductions, and failing to report all income, as these can lead to higher taxes or penalties.